Stochastic Volatility model¶

In [1]:

import numpy as np

import pymc3 as pm

from pymc3.distributions.timeseries import GaussianRandomWalk

from scipy import optimize

%pylab inline

Populating the interactive namespace from numpy and matplotlib

Asset prices have time-varying volatility (variance of day over day

returns). In some periods, returns are highly variable, while in

others very stable. Stochastic volatility models model this with a

latent volatility variable, modeled as a stochastic process. The

following model is similar to the one described in the No-U-Turn Sampler

paper, Hoffman (2011) p21.

Here, \(y\) is the daily return series and \(s\) is the latent log volatility process.

Build Model¶

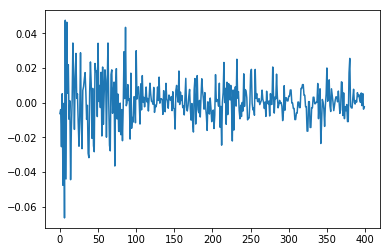

First we load some daily returns of the S&P 500.

In [2]:

n = 400

returns = np.genfromtxt(pm.get_data("SP500.csv"))[-n:]

returns[:5]

Out[2]:

array([-0.00637 , -0.004045, -0.02547 , 0.005102, -0.047733])

In [3]:

plt.plot(returns)

Out[3]:

[<matplotlib.lines.Line2D at 0x7fae8c869a20>]

Specifying the model in pymc3 mirrors its statistical specification.

In [4]:

model = pm.Model()

with model:

sigma = pm.Exponential('sigma', 1./.02, testval=.1)

nu = pm.Exponential('nu', 1./10)

s = GaussianRandomWalk('s', sigma**-2, shape=n)

r = pm.StudentT('r', nu, lam=pm.math.exp(-2*s), observed=returns)

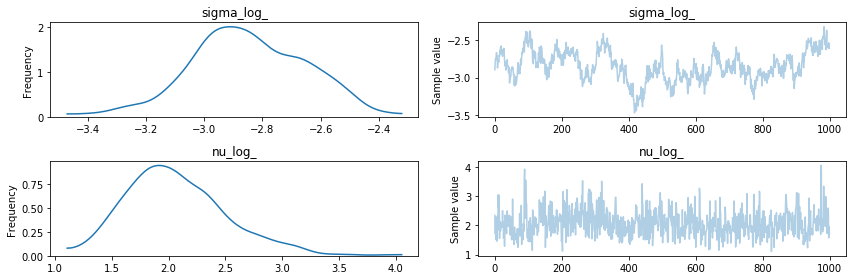

Fit Model¶

For this model, the full maximum a posteriori (MAP) point is degenerate and has infinite density. To get good convergence with NUTS we use ADVI (autodiff variational inference) for initialization.

In [9]:

with model:

trace = pm.sample(2000, tune=1000)[1000:]

Auto-assigning NUTS sampler...

Initializing NUTS using ADVI...

Average Loss = 7.9136: 100%|██████████| 200000/200000 [01:14<00:00, 2691.66it/s]

Finished [100%]: Average Loss = 7.896

100%|██████████| 2000/2000 [04:47<00:00, 8.48it/s]/home/jovyan/pymc3/pymc3/step_methods/hmc/nuts.py:255: UserWarning: Chain 0 reached the maximum tree depth. Increase max_treedepth, increase target_accept or reparameterize.

'reparameterize.' % chain)

/home/jovyan/pymc3/pymc3/step_methods/hmc/nuts.py:268: UserWarning: The acceptance probability in chain 0 does not match the target. It is 0.688505126364, but should be close to 0.8. Try to increase the number of tuning steps.

% (chain, mean_accept, target_accept))

In [10]:

figsize(12,6)

pm.traceplot(trace, model.vars[:-1]);

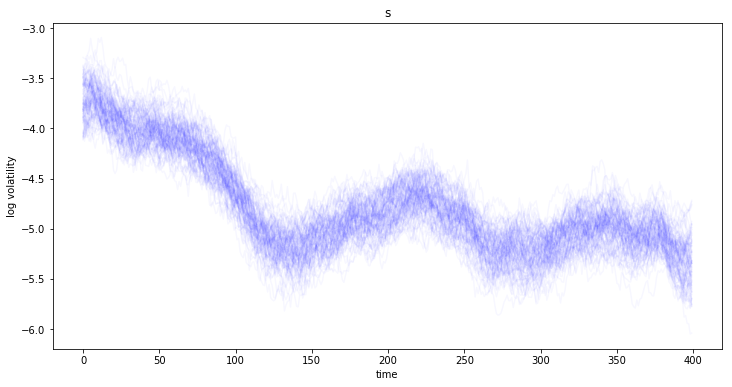

In [11]:

figsize(12,6)

title(str(s))

plot(trace[s][::10].T, 'b', alpha=.03);

xlabel('time')

ylabel('log volatility')

Out[11]:

<matplotlib.text.Text at 0x7fae6019f8d0>

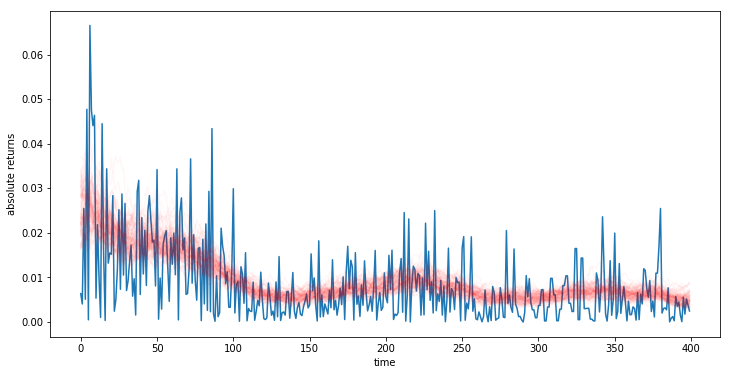

Looking at the returns over time and overlaying the estimated standard deviation we can see how the model tracks the volatility over time.

In [12]:

plot(np.abs(returns))

plot(np.exp(trace[s][::10].T), 'r', alpha=.03);

sd = np.exp(trace[s].T)

xlabel('time')

ylabel('absolute returns')

Out[12]:

<matplotlib.text.Text at 0x7fae64197c50>

References¶

- Hoffman & Gelman. (2011). The No-U-Turn Sampler: Adaptively Setting Path Lengths in Hamiltonian Monte Carlo.